Generational planning (or “estate planning”) is the process of planning to pass your wealth on to future generations – usually to family – in the most tax efficient way possible.

It can be hard to know where to begin, especially when it’s a subject that comes with a lot of emotion attached. But as we’ve discussed time and time again, planning and readiness is crucial – you can’t leave it to chance.

So, to help you get started, here are four key elements of generational planning that could help you on your way.

1. Saving for their future

When I was born, my parents set up a credit union account. They periodically saved into it so that, once I reached 18, I had a cushion of wealth. This was common and still is, whether it be a credit union or bank account.

Although opened with good intentions, leaving money in a traditional bank account or credit union for 18+ years has negative impacts affecting the future spending power. The main culprits include inflation and account fees. Interest rates have been typically low in recent years, which means growth is minimal from the outset.

Just think – if inflation is 5% but your interest rate is only 2%, you are losing 3% before you even consider the impact of bank charges.

My own first memory of savings was getting a £1 from my Mum on a Friday morning to buy Sammy Stamps (saving stamps from the credit union). I will never forget the sense of satisfaction when I filled my first full book of stamps and the absolute horror when I realised that my yogurt had burst in my schoolbag.

You could say that was my first exposure to a drop in share value – although the cashier in the credit union was very nice and accepted my soggy, strawberry-flavoured stamps!

There are many other, more effective ways to save for a child’s future which make the money work as hard for you as possible. I will briefly touch on a few below.

2. Small Gift Exemption

Anyone can gift someone else up to €3,000 per year tax free, regardless of their relationship.

For example: a grandparent with 3 children and 7 grandchildren could gift each person €3,000 and pass on €30,000 in one year tax-free to the next generation.

Those funds can be invested without the children’s knowledge, who cannot access the funds until they turn 18.

Unlike an insurance policy or other types of gifting contracts, you are not obliged to keep up these payments every year. Therefore, you have complete control over the flow of wealth to the next generation.

3. Inheritance

If you have received a gift or inheritance, it is likely you will be liable for inheritance tax (Capital Acquisitions Tax, or CAT). The liability is determined by the relationship to the person you have received the gift or inheritance from. At the time of writing, the current thresholds for inheritance tax are detailed below.

| Group A: €335,500 | Group B: €32,500 | Group C: €16,250 |

| Applies where the beneficiary is a child (including adopted child step-child, and certain foster children) or a minor child of a deceased child of the disponer. Parents also fall within this threshold where they take an inheritance of an absolute interest from a child. | Applies where the beneficiary is a brother, sister, niece, nephew or lineal ancestor or lineal descendant of the disponer. | Applies in all other cases. |

These are lifetime limits and there are a few exemptions. Therefore, I would urge you to speak to a financial planner or tax advisor about your personal circumstances.

The taxation liability can be 30% or 33% tax depending on your personal circumstances. The receiver is liable for the tax, not the person giving the gift or inheritance.

At first glance, one would be forgiven to think this amount will more than cover the inheritance bill.

Let’s look at a fictional family of 4, comprising of two parents and two school going children. In our example, they have:

-

• property (€400,000)

• cars (€35,000)

• savings (€150,000)

• investments (€75,000)

• pensions (€150,000)

• life cover (€200,000)

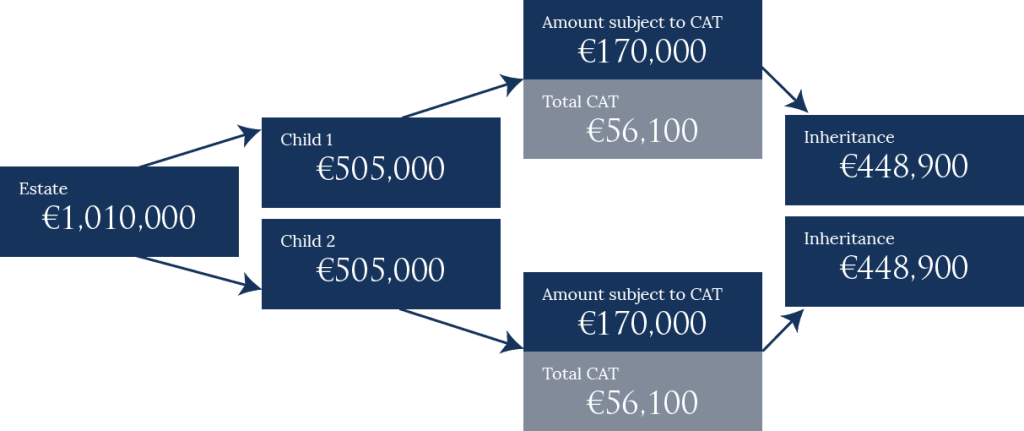

Let’s assume the parents split their entire estate of €1,010,000 equally between both children – €505,000 per child. The children will be liable to pay Capital Acquisitions Tax at 33%, on the amount over their appropriate threshold, which is €335,000.

Therefore, a tax liability will exist of €56,100 and the inheritance which was €505,000 has now dropped to €448,900.

In this scenario, the children have the funds to cover the tax liability. However, if the inheritance was mostly property, they might be forced to sell the property to release cash. The infographic below provides a quick snapshot of this.

4. Section 72

Inheritance tax is payable in one lump sum within a limited period from the time of the inheritance. A ‘Section 72’ policy can solve the immediate concern of what to do when you receive an inheritance from a loved one in one hand, and a large CAT Bill in the other.

A ‘Section 72’ is a whole-of-life insurance policy, the proceeds of which are tax-free if used to pay an inheritance tax bill.

We can help you calculate the value of your estate and if there is any inheritance tax liability. Once you know the value of the liability, you can take out an insurance policy to cover this liability. On your death, the proceeds of this plan will pay the inheritance tax bill so your children can inherit your estate tax-free. One of our Private Client Managers, Paddy Andrews, recently wrote in detail about how Section 72 policies work – you can read it here.

What next?

If this article has struck a chord with you, please do get in touch with us over email at info@metisireland.ie, or by phone on 01 908 1500.

Mary Carney

Financial Planner

Disclaimer

Metis Ireland Financial Planning Ltd t/a Metis Ireland is regulated by the Central Bank of Ireland.

All content provided in these blog posts is intended for information purposes only and should not be interpreted as financial advice. You should always engage the services of a fully qualified financial adviser before entering any financial contract. Metis Ireland Financial Planning Ltd t/a Metis Ireland will not be held responsible for any actions taken as a result of reading these blog posts.