Within the Financial Services industry, ESG (Environmental, Social and Governance) has been a hot topic of discussion over the last number of years. However, due to restrictions on the comparison of funds, and false or not-so-honest claims of sustainability (known as ‘greenwashing’), investors and advisors have tended to disregard it. My colleague Cian wrote a blog on the ‘greenwashing’ phenomenon last year, which you can read here.

Over the last five years, the EU has worked extensively to regulate and bring some consistency to the way that ESG funds are compared and rated. These regulations take the 10 action points from the 2018 European Commission Action Plan: Financing Sustainable Growth as their basis.

Over the next few months, I’ll explain the various regulations and initiatives which have been introduced in recent years and what they mean for you.

Today we’ll start with two of the regulations around transparency and disclosures within ESG funds. These are:

• EU Taxonomy. This is a classification system for economic activity.

• SFDR (Sustainable Finance Disclosure Regulation). This is how financial market participants and financial advisors disclose how they use ESG.

It can get a little technical and jargon-y, but bear with me.

What is ESG?

Let’s start with the basics.

ESG may seem like a new-fangled concept. However, ESG investing has been around since the 1960s, when it was known at the Socially Responsible Investment (SRI) Movement. It then became known as ESG in the early 2000s. In a nutshell, this type of investing is “a set of standards for a company’s behaviour used by socially conscious investors to screen potential investments”.

ESG consists of three pillars: Environmental, Social and Governance.

‘Environmental’ covers what you’d imagine it does – how companies interact with and impact the natural world. ‘Social’ refers to things such as labour standards, diversity and inclusion policies, human rights, and product safety. Lastly, ‘Governance’ focuses on the leadership and management practices of companies.

In short, it’s simply Planet, People, and Profit.

People tend to use the terms ‘ESG’ and ‘Sustainable’ interchangeably when talking about investments. However, they’re actually two very different things with different regulatory requirements.

What decides a fund’s level of sustainability?

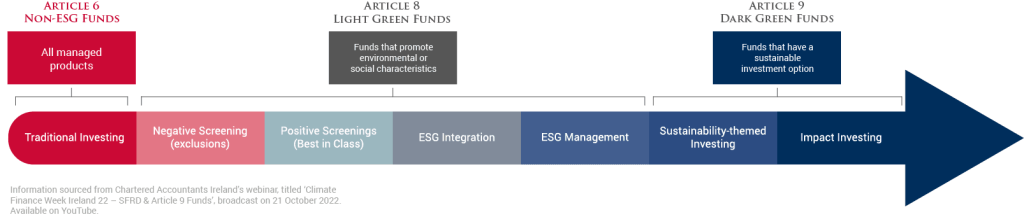

Sustainable Finance Disclosure Regulation (SFDR) is a set of disclosure requirements, introduced for two key reasons: improving transparency in the market for sustainable investment products, and preventing greenwashing.

It’s designed to standardise the way that financial market participants and financial advisors disclose how they use ESG. In other words, it’s a consistent set of rules about whether or not they’re allowed to describe their funds as “Sustainable”.

As per these regulations, fund managers must disclose detailed information to support their claim that a fund is sustainable. That information is then evaluated against the SFDR parameters, which decides whether a fund is classified as Article 6, 8 or 9.

The SFDR I and II classifications were introduced in 2021 and 2023. The most recent parameters are significantly more restrictive in their definitions of what can and can’t be classed as sustainable. This has resulted in almost €300 billion worth of funds being downgraded from Article 9 to Article 8 since the introduction of the classifications in 2021, meaning that these funds are no longer considered “Sustainable” – just “General ESG”. That’s some serious reclassification! The bar is getting higher.

The EU Taxonomy standardises the language we use to talk about ESG

The EU Taxonomy is another regulatory framework that aims to promote sustainable investments within the EU. It draws on scopes of the SFDR (as discussed above) and the EU Non-Financial Reporting Directive (NFRD), which I’ll cover in next month’s article, to define its own scope. The Taxonomy requires additional disclosures from financial market participants and large companies to those laid out in the SFDR and NFRD.

The Taxonomy is a green classification system. It determines whether or not an economic activity is environmentally sustainable. This helps investors, companies, and policy makers to make more informed decisions, as it identifies activities that it believes will make substantial contributions to environmental objectives. In turn, this helps to finance the transition to a more sustainable economy.

By defining what’s “green” or “sustainable”, the EU Taxonomy creates a common language for sustainability that sets strict standards to prevent greenwashing.

Its classification system covers six topics:

1. Climate change mitigation

2. Climate change adaptation

3. Sustainable use and protection of water and marine resources

4. Transition to a circular economy

5. Pollution prevention and control

6. Protection and restoration of biodiversity and ecosystems

To be acceptable under the EU Taxonomy, an economic activity must to contribute to one of the above environmental objectives. Additionally, it must also ensure that it doesn’t cause significant harm to any of the others.

Difficulties with standardising ESG definitions

Some groups are criticising the EU Taxonomy. The most prominent of these are Greenpeace, Friends of the Earth Germany, Transport & Environment and Client Earth. Their criticism is that gas and nuclear energy are both on the EU’s list of investments permitted to be labelled as ‘green’.

Greenpeace said it would file a lawsuit at the EU’s top court in April. Its grounds are that the CO2 emissions limits for gas power plants are too loose for the EU to achieve its climate goals.

This example illustrates the difficulties involved as we attempt to settle on a universal definition of what constitutes “green” or “sustainable” investing.

Despite the extensive work from the EU to improve transparency and raise standards of green and sustainable funds, there’s clearly still work to be done to bring standards in line with consumer expectations. But as such a volatile, emotive, and complex topic, can that even be achieved? Time will tell.

Next in the series

The rising standards within the industry of what constitutes an ESG fund has inevitably caused to many funds which met previous benchmarks to be downgraded as requirements tighten.

It’s getting harder and harder for companies to “greenwash” themselves – and that can only be a good thing.

My next blog explores greenwashing, Non-Financial Reporting Directive (NFRD), Corporate Social Reporting Directive (CSRD).

Mary Carney

Financial Planner

Sources:

https://www.eurosif.org/policies/sfdr/

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52018DC0097&from=EN

https://www.morningstar.co.uk/uk/news/231438/esg-fund-downgrade-accelerates.aspx

https://www.youtube.com/watch?v=dTFl-Ew0pAU

Disclaimer

Metis Ireland Financial Planning Ltd t/a Metis Ireland is regulated by the Central Bank of Ireland.

All content provided in these blog posts is intended for information purposes only and should not be interpreted as financial advice. You should always engage the services of a fully qualified financial adviser before entering any financial contract. Metis Ireland Financial Planning Ltd t/a Metis Ireland will not be held responsible for any actions taken as a result of reading these blog posts.