Whether directly or indirectly, we all know someone who’s been affected by the recent wave of redundancies announced over the last number of months.

No doubt it is an unsettling time for those of you impacted directly by a business restructure. But we’ve worked with many individuals in this position. We’ve helped them to pick up the pieces and plan their future finances. From that experience, we’re here to tell you that:

-

a) it’s okay to be worried, and

b) although it may feel like there’s nothing you can do to make things better, we assure you there’s more in your power than you think. We can help you with that.

Now, you’ll have questions – what happens to my pension now? What are the consequences of getting extra cash now vs later? Have I enough money for the future?

These are all important questions, but first it’s important to understand what the different redundancy packages entail.

Your Redundancy Entitlements Explained

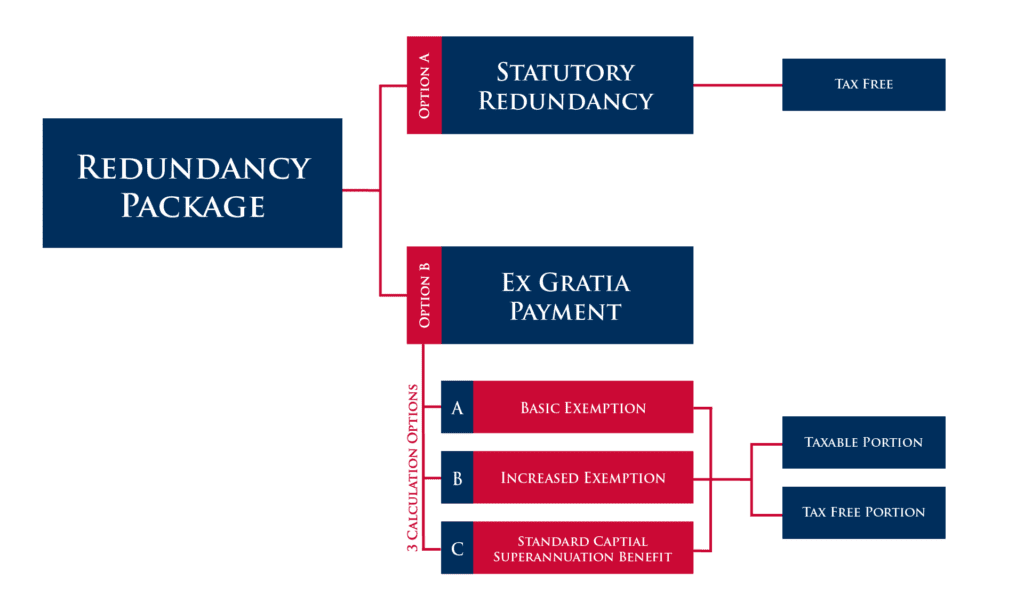

There is a maximum lifetime limit of €200,000 on all termination payments received. A Redundancy Package can be broken down into Statutory and Ex Gratia Payments:

Statutory Redundancy Entitlement

This is a minimum compulsory entitlement under revenue rules that a company is obliged to offer its staff. The employee receives all these funds tax-free.

This figure is calculated as follows:

2 weeks’ pay for each complete year service + 1 further week’s pay.

The amount of statutory redundancy is subject to a maximum earnings limit of €600 per week (€31,200 per year).

Statutory redundancy only applies to employees with two years’ service.

Ex Gratia Payment

Lump sum payments received from an employer on redundancy may be taxable.

The amount which you can receive tax free depends on which of the 3 options listed below that you choose:

-

Basic Exemption:

€10,160 + €765 for each complete years’ service with the employer.

Increased Exemption:

An additional €10,000 is added to the calculation if not claimed within the previous 10 years. This amount is reduced by the amount of the future tax-free pension lump sum.

Standard Capital Superannuation Benefit (SCSB):

This is calculated as follows:

Pension Implications

Once you have received a redundancy offer from your employer, you will need to carefully consider the tax treatment of your redundancy payment.

Your decision can have a significant impact on the tax-free lump sums that you qualify for from both your redundancy package and your pension entitlements.

You should avail of independent advice before deciding or signing any employer’s offer.

What next?

We would like to assist in any way we can. Here at Metis Ireland, we have a wealth of experience and expertise in advising on the financial impact of redundancy. Our team of financial planners can advise you on the options available to you on your redundancy package.

In addition to acting as a soundboard for more generic questions, we can model your cashflow position to provide you with some peace of mind going forward until the next step in your career.

If you have received a redundancy offer and wish to clarify the best option for you, contact us by phone on 01 908 1500 or by email at info@metisireland.ie.

Disclaimer

Metis Ireland Financial Planning Ltd t/a Metis Ireland is regulated by the Central Bank of Ireland.

All content provided in these blog posts is intended for information purposes only and should not be interpreted as financial advice. You should always engage the services of a fully qualified financial adviser before entering any financial contract. Metis Ireland Financial Planning Ltd t/a Metis Ireland will not be held responsible for any actions taken as a result of reading these blog posts.