Over the last few weeks, we’ve been telling anyone who would listen about the wonders of Personal Retirement Savings Accounts (PRSAs) and the how the recent changes in legislation have made then even more wonderous (Wonderous-er? Wonderous-est? Wonder-ifique? We’ll get back to you on that one…).

But how exactly can this benefit you? Well, today we’re looking at a case study for the self-employed, which includes sole traders and partners. This should give you an idea of what a PRSA could look like in practice for those of you who fall into the self-employed bracket.

The Background

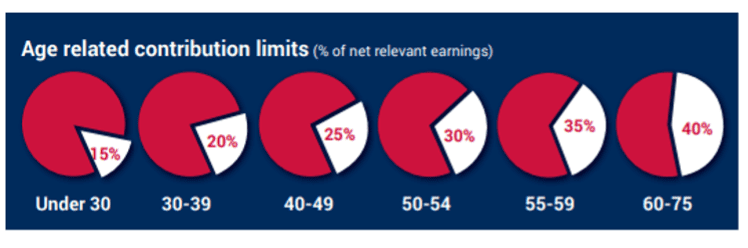

There are many advantages to being self-employed. However, one significant drawback is that all your business profit is taxed as income in your hands. You can make pension contributions and claim tax relief, but these are limited to a percentage of your earnings up to €115,000.

The rates are outlined in the graphic below.

The Scenario

Let’s take a self-employed solicitor whose gross taxable income is over €600,000 per annum. They’re 52 and married.

They can still only contribute up to 30% of €115,000 (€34,500) to a pension, resulting in tax relief of €13,800. This is unchanged from previous years.

This same solicitor employs their spouse as a bona fide secretary within their business and pays them a salary of €30,000 per annum. Their spouse is now an employee and therefore entitled to receive employer pension contributions.

As per our previous article, there’s no limit or benefit-in-kind (BIK) on employer pension contributions to a PRSA for any of their employees.

The Solution

-

• Both spouses set up PRSAs.

• The self-employed solicitor makes an annual contribution of €34,500 and claims 40% tax relief.

• They also make an employer contribution of €100,000 to their spouse’s PRSA. They’ll effectively get tax relief from Income tax, PRSI and USC or approximately 52% tax relief.

Want to know more about you might avail of this opportunity?

Before making any decisions, we always strongly recommend that you seek advice from a qualified, experienced professional.

This could be:

-

• Whoever does your business accounts

• An independent tax advisor

• A pensions and financial planning expert, such as Metis Ireland

If you’d like to discuss your situation and your plans for your pension fund, please do get in touch with us over email at info@metisireland.ie, or by phone on 01 908 1500.

Cian Callaghan

Private Client Manager

Disclaimer: Metis Ireland is not a tax advisor. All content in these blog posts is intended for information purposes only. We recommend that you should always seek independent tax advice.

Disclaimer

Metis Ireland Financial Planning Ltd t/a Metis Ireland is regulated by the Central Bank of Ireland.

All content provided in these blog posts is intended for information purposes only and should not be interpreted as financial advice. You should always engage the services of a fully qualified financial adviser before entering any financial contract. Metis Ireland Financial Planning Ltd t/a Metis Ireland will not be held responsible for any actions taken as a result of reading these blog posts.