For senior executives with vested or unvested shares, RSUs or other equity compensation, making informed decisions is essential to protect and grow your wealth.

Ireland is home to many of the worlds largest tech and pharma companies and as a result we have seen a massive increase in employees receiving shares as part of their overall compensation package. Seeing those shares vest can feel like a bonus, especially when the share price is on the rise. However, inaction here could be exposing you to significant and unnecessary financial risk.

In this article we will explore why diversifying your stock holdings and building a well-rounded portfolio is a far more prudent strategy for long-term financial security.

The Illusion of Control

It’s natural to feel a strong connection to the company you contribute to daily. You understand its products, its culture, and perhaps even its future potential. This familiarity can create a sense of comfort and even overconfidence in the company’s continued success. There can be an element of “stick to what you know”.

However, the market is complex and unpredictable. Even the most innovative and successful companies face unforeseen challenges:

- Industry Shifts: Technological disruptions, regulatory changes, and the emergence of new competitors can drastically alter a company’s trajectory, regardless of its current dominance.

- Company-Specific Risks: Internal issues, management changes, product failures, or even negative press can send a stock price tumbling, irrespective of broader market conditions.

- Market Volatility: External economic factors, geopolitical events, and investor sentiment can impact even the strongest stocks.

Too big to fail?

You only have to look at companies like Kodak, Nokia or Yahoo who were once the titans in their industries only to have their businesses disrupted by technology and competition.

- Kodak, for much of the 20th century, dominated the photographic film market. Despite inventing the first digital camera in 1975, they clung too tightly to their lucrative film business. As digital cameras became mainstream, Kodak struggled to adapt, eventually filing for bankruptcy in 2012.

- Nokia was the undisputed market leader in the mobile phone market, however, the rise of the smartphone, spearheaded by Apple’s iPhone and the Android operating system, caught Nokia off guard.

- In the early days of the internet, Yahoo was a leading search engine, web portal, and technology company. It had numerous opportunities to acquire companies that would later become giants, such as Google. However, a series of missteps, missed opportunities, and a failure to adapt led to its decline. Yahoo, who was once valued at over $125bn in the early 2000s, sold its operating business to Verizon in 2017 for around $4.8bn, a fraction of what it was once valued at.

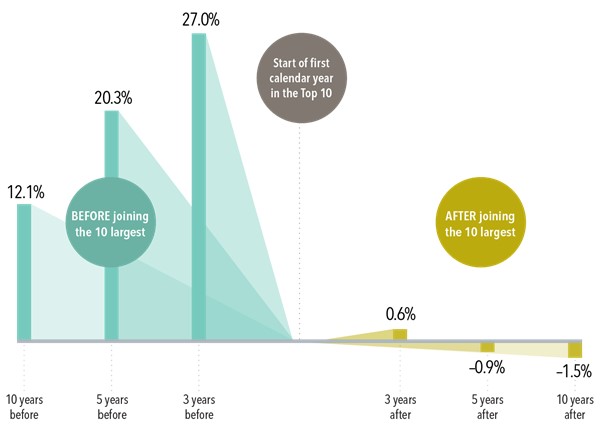

While it often seems some companies are too big to fail, and the growth they have experienced will continue indefinitely, history tells a different story. Dimensional research team analysed the performance of the top 10 stocks in the S&P 500 index in the years prior to joining the top 10, and then after joining. The performance on the way to the top is unsurprisingly impressive but the bigger you get the harder it can be to keep generating impressive growth figures. As a result between 1927 and 2022 research found that the top 10 stocks on average underperform the index once they reach the top, eventually getting replaced by new companies.

Annualized returns in excess of the US market before and after joining the top 10 largest US stocks, January 1927–December 2022

For employees holding a significant amount of their company’s stock, these historical examples serve as a powerful reminder of the inherent risks of over-concentration. While your current employer may be a leader in its field today, the future is uncertain. Diversifying your holdings is not a bet against your company, it’s a strategic move to protect your financial well-being against unforeseen disruptions to one industry or company.

The Danger of Over-Concentration: All Your Eggs in One Basket

Holding a large percentage of your wealth in your employer’s stock creates a significant exposure to that company. If your company faces financial difficulties, you could not only lose your job but also see a significant decline in the value of your stock holdings simultaneously. This double whammy can have a major impact on your financial state.

Behavioural challenges in deciding what to do

- ‘Fomo’ can play a big part in this decision. When you see the stock rise, the fear of selling and missing out on future gains can be a major roadblock to a sensible decision, especially when it seems like all your colleagues are ‘all in’.

- Procrastinating: the first step to understand how you actually go about selling shares, can be a major hurdle.

- Tax payment: Not wanting to sell due to tax on gains

- Status Quo: Make no decision for fear of making the wrong one

Understanding your behavioural biases might be the most important aspect of managing your money. For me it all comes down to one simple question, if you currently have lets say €500,000 savings sitting in cash in your bank account, would you invest all of that €500,000 into the company where you work? By not making a decision to sell your stock, you are effectively making this decision to invest all your savings into one stock.

A prudent approach

- Understand Your Risk Tolerance and Financial Goals. What are your short-term and long-term financial objectives? Once you know this you can assess how much money you may need in the short term and how much risk capacity you have.

- Behavioural Biases: ‘Fomo’ can play a big part

- Establish an Investment Strategy: Determine an appropriate investment portfolio based on your risk tolerance and goals. You may want to meet with a financial adviser to put this in place.

- Develop a selling plan: Don’t try and time the market here. Instead, consider a systematic approach to selling your vested shares over time. This could involve selling a certain percentage each quarter or year.

- Tax: Understand the tax environment. While selling shares usually operates on a first in first out (FIFO) basis meaning you must sell the units you received first, some companies provide a small window where you can sell the most recent vested units first usually just after they have vested. Because of the FIFO method, many people will have a significant tax bill to pay when they sell. I would encourage you to think positively about this and that paying tax means you have made a gain.

Disclaimer

Metis Ireland Financial Planning Ltd t/a Metis Ireland is regulated by the Central Bank of Ireland.

All content provided in these blog posts is intended for information purposes only and should not be interpreted as financial advice. You should always engage the services of a fully qualified financial adviser before entering any financial contract. Metis Ireland Financial Planning Ltd t/a Metis Ireland will not be held responsible for any actions taken as a result of reading these blog posts.