When it comes to investing your money, “risk” gets all the negative press. But little do investors realise that there’s a far more nefarious foe out there which poses the real risk to your cash savings: inflation.

There’s a good reason that #3 of our Investment Philosophy is “beware the real risk: inflation”. This is important stuff.

Inflation and retirement planning

As part of retirement planning, you’ll need to take stock of your assets and work out how your money is currently spread across the main asset classes – these are cash, property, shares, bonds, and alternatives.

Any financial planner worth their salt will balance your assets in a way that will best help you achieve your retirement goals. What’s the best way to make sure that you can help the kids with house deposits? How can we make sure you can afford to visit your family in Colorado every year? When do we need to make funds available to purchase a holiday home?

This is where the conversation of risk comes in. “Risk” is mostly confused with volatility, which is the norm when invested in the great companies of the world – that is, the stock market. However, the real risk is the risk of running out of money. Your financial plan and your financial planner will help you map this out and avoid this scenario. In essence, your financial plan will answer the question: “Are we going to be ok?”

Now, many couples hold on to a belief that cash is king, and that holding as much cash in savings as possible is the most secure way to enact their plans and minimise risk. This couldn’t be further from the truth. The real risk is not growing your money enough to reach your goals.

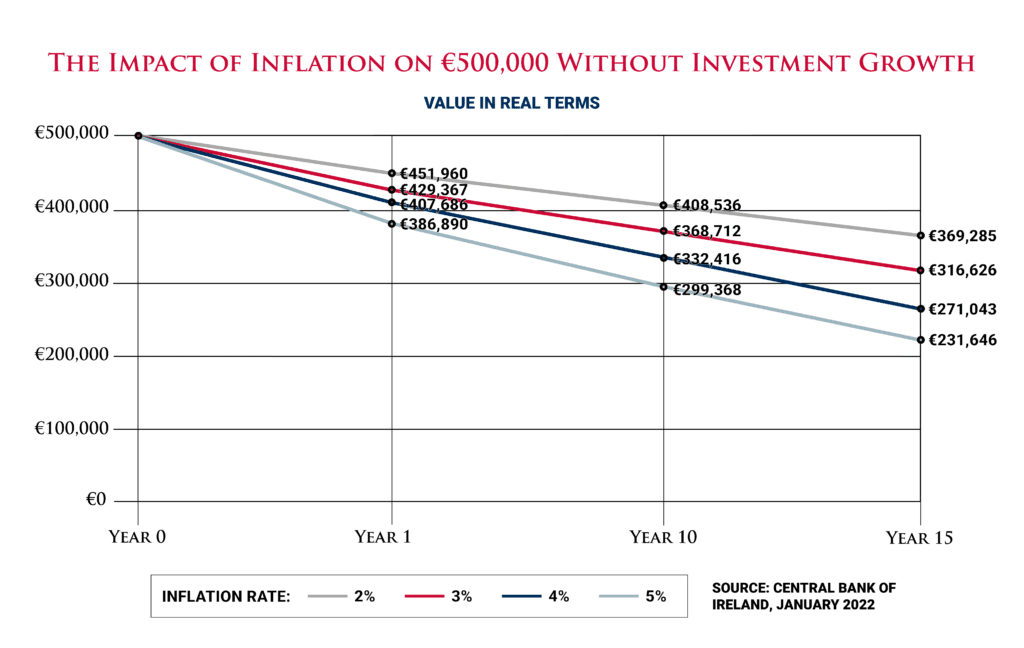

What will inflation do to my savings?

If you’ve left all your money in cash savings, or if you’ve defaulted to the super-cautious investment approach in your pension scheme, there’s a real risk that inflation could eat away huge swathes of your money’s purchasing power. That’s effectively returning a loss, even though it may not look like it.

Figures from the Central Bank of Ireland from January this year show that the purchasing power of a €500,000 saved sum at today’s typical interest rate (nil), and at an inflation rate of 5%, would incur a real-terms loss of:

-

• more than €110,000 over five years

• over €200,000 after ten years

• an eye-watering €270,000 over 15 years.

Even at an inflation rate of only 1%, you’d still experience your purchasing power decline to a real-terms loss of almost €100,000 over ten years.

And these are just illustrative examples. Forecasts are expecting inflation in Ireland to average at 8.1% in 2022 and 6.9% in 2023. That’s off this chart!

If you saw those figures marked as losses on an investment, you’d be worried. But inflation is a silent drain on your cash savings. Arguably, it’s the riskiest “savings” option.

Of course, it is important to have access to cash savings on hand for emergencies and for more immediate expenses that may occur. When we’re talking about putting money into investments, we’re looking to the long term – five years and more. Our experience tells us most people invest for multi-decade time frames! We won’t encourage you to invest anything that we forecast you’ll need in the shorter term.

Why plan?

When you decide to buy a new car, you don’t just sit around and hope that the exact model you want will turn up on your driveway, ready and paid for. It’s a purchase that you take seriously – you do your due diligence, research the latest models, find a dealership you like and trust, take a few test drives, arrange your finances to make room for the expense of it.

Now, compared to retirement, a car is relatively small beans. And yet, I’d be willing to bet that most people have put more thought into their new Audi than into the most free and expansive stretch of time in your life. When you retire, you’ve got a solid couple of decades ahead of you which you’ll want to fill with enjoyable, meaningful experiences and a standard of living that you’re happy with. This doesn’t just happen without foreplanning – there is no magic retirement fairy who will do it for you. The simple fact of the matter is, if you don’t do it, it won’t happen.

If you want to give yourself the best chance of achieving your dream retirement, it’s essential that your money is managed to reflect how you plan to use your assets in the future.

Get in touch with us if you want to know more about starting your own retirement plan.

Carl Widger

Managing Director

Disclaimer

Metis Ireland Financial Planning Ltd t/a Metis Ireland is regulated by the Central Bank of Ireland.

All content provided in these blog posts is intended for information purposes only and should not be interpreted as financial advice. You should always engage the services of a fully qualified financial adviser before entering any financial contract. Metis Ireland Financial Planning Ltd t/a Metis Ireland will not be held responsible for any actions taken as a result of reading these blog posts.